All Categories

Featured

Table of Contents

There are three types of annuities: taken care of, variable and indexed. With a fixed annuity, the insurance policy business guarantees both the price of return (the rate of interest) and the payment to the capitalist. The passion price on a fixed annuity can change in time. Frequently the passion rate is repaired for a number of years and after that modifications occasionally based upon existing prices.

With a deferred fixed annuity, the insurance provider agrees to pay you no much less than a specified interest rate throughout the time that your account is expanding. With an instant set annuityor when you "annuitize" your postponed annuityyou receive a predetermined fixed quantity of money, typically on a regular monthly basis (comparable to a pension plan).

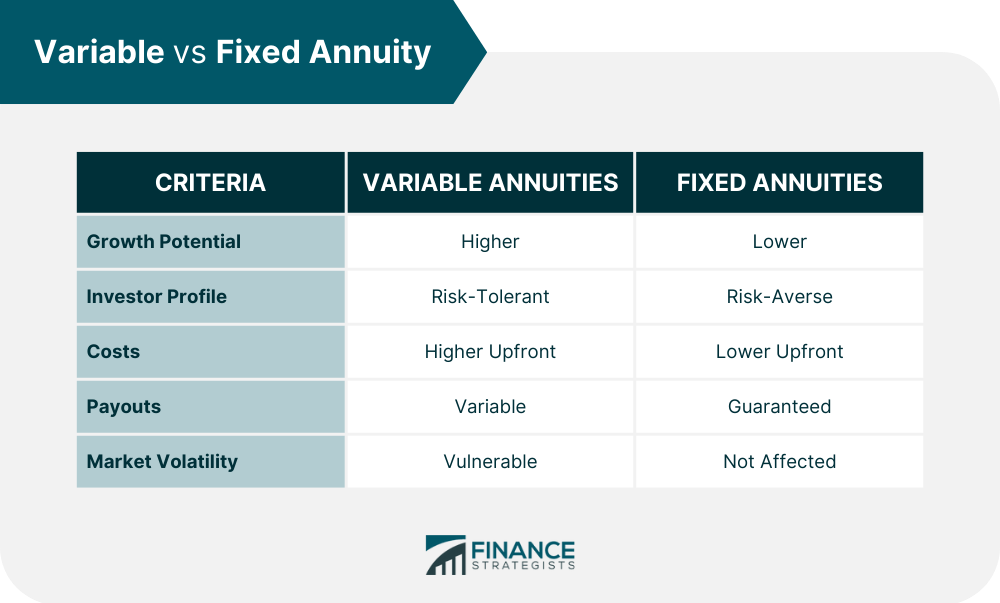

While a variable annuity has the benefit of tax-deferred development, its annual expenses are most likely to be a lot greater than the costs of a typical common fund. And, unlike a taken care of annuity, variable annuities do not provide any kind of warranty that you'll gain a return on your financial investment. Instead, there's a threat that you could actually shed cash.

Analyzing Annuities Fixed Vs Variable A Comprehensive Guide to Investment Choices Breaking Down the Basics of Investment Plans Pros and Cons of Deferred Annuity Vs Variable Annuity Why Choosing the Right Financial Strategy Matters for Retirement Planning How to Compare Different Investment Plans: How It Works Key Differences Between Variable Annuities Vs Fixed Annuities Understanding the Key Features of Tax Benefits Of Fixed Vs Variable Annuities Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Retirement Income Fixed Vs Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

Because of the intricacy of variable annuities, they're a leading resource of capitalist grievances to FINRA. Prior to purchasing a variable annuity, thoroughly read the annuity's prospectus, and ask the person selling the annuity to explain every one of the item's attributes, bikers, prices and constraints. You must likewise know how your broker is being made up, consisting of whether they're receiving a payment and, if so, just how much.

Indexed annuities are intricate financial tools that have features of both dealt with and variable annuities. Indexed annuities normally supply a minimum surefire rates of interest incorporated with a passion price linked to a market index. Numerous indexed annuities are linked to broad, well-known indexes like the S&P 500 Index. Some use other indexes, including those that stand for various other sectors of the market.

Comprehending the features of an indexed annuity can be complex. There are several indexing approaches firms use to compute gains and, as a result of the range and complexity of the methods used to credit report interest, it's hard to contrast one indexed annuity to one more. Indexed annuities are generally classified as one of the complying with two kinds: EIAs supply a guaranteed minimum rate of interest (usually at the very least 87.5 percent of the premium paid at 1 to 3 percent rate of interest), along with an extra rate of interest connected to the performance of one or even more market index.

Conservative financiers who value safety and security and stability. Those nearing retired life who desire to sanctuary their possessions from the volatility of the supply or bond market. With variable annuities, you can buy a selection of protections including stock and bond funds. Stock market performance identifies the annuity's worth and the return you will certainly receive from the cash you invest.

Comfy with changes in the stock exchange and want your financial investments to keep speed with rising cost of living over an extended period of time. Youthful and want to prepare monetarily for retirement by reaping the gains in the stock or bond market over the long-term.

As you're developing your retirement financial savings, there are numerous methods to stretch your money. can be particularly helpful financial savings tools since they guarantee an earnings quantity for either a collection period of time or for the remainder of your life. Taken care of and variable annuities are two choices that offer tax-deferred development on your contributionsthough they do it in different means.

Understanding Financial Strategies A Closer Look at How Retirement Planning Works What Is Fixed Vs Variable Annuity? Benefits of Pros And Cons Of Fixed Annuity And Variable Annuity Why Choosing the Right Financial Strategy Can Impact Your Future How to Compare Different Investment Plans: Explained in Detail Key Differences Between Different Financial Strategies Understanding the Key Features of Fixed Annuity Or Variable Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Variable Annuity Vs Fixed Indexed Annuity A Beginner’s Guide to Variable Vs Fixed Annuities A Closer Look at Variable Vs Fixed Annuity

variable annuity or both as you plot out your retirement revenue strategy. An offers a guaranteed rate of interest. It's taken into consideration a conventional item, offering a modest incomes that are not tied to market performance. Your agreement value will certainly increase because of the amassing of guaranteed passion earnings, meaning it will not decline if the marketplace experiences losses.

An includes purchased the stock market. Your variable annuity's investment efficiency will impact the size of your savings. It might assure you'll get a collection of payouts that begin when you retire and can last the remainder of your life, given you annuitize (begin taking settlements). When you begin taking annuity payments, they will certainly depend on the annuity value during that time.

Market losses likely will cause smaller payouts. Any kind of interest or various other gains in either type of contract are protected from current-year tax; your tax liability will certainly come when withdrawals begin. Allow's look at the core features of these annuities so you can determine how one or both may fit with your overall retirement method.

:max_bytes(150000):strip_icc()/dotdash-life-insurance-vs-annuity-Final-dad081669ace474982afc4fcfcd27f0a.jpg)

A set annuity's worth will not decline because of market lossesit's regular and steady. On the other hand, variable annuity values will change with the efficiency of the subaccounts you choose as the marketplaces fluctuate. Profits on your dealt with annuity will very rely on its acquired price when bought.

On the other hand, payout on a fixed annuity purchased when rate of interest are low are more probable to pay out earnings at a reduced rate. If the rates of interest is assured for the length of the agreement, incomes will continue to be continuous despite the markets or rate task. A fixed price does not suggest that taken care of annuities are safe.

While you can not land on a fixed rate with a variable annuity, you can pick to purchase traditional or aggressive funds tailored to your danger degree. Extra conservative investment alternatives, such as temporary mutual fund, can help minimize volatility in your account. Considering that repaired annuities use an established price, reliant upon present rate of interest, they don't offer that same adaptability.

Decoding Variable Annuities Vs Fixed Annuities A Closer Look at What Is A Variable Annuity Vs A Fixed Annuity What Is Retirement Income Fixed Vs Variable Annuity? Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Matters for Retirement Planning How to Compare Different Investment Plans: A Complete Overview Key Differences Between Variable Annuity Vs Fixed Indexed Annuity Understanding the Risks of Fixed Index Annuity Vs Variable Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Vs Variable Annuity Pros Cons FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Fixed Income Annuity Vs Variable Growth Annuity A Beginner’s Guide to Annuities Fixed Vs Variable A Closer Look at Variable Annuities Vs Fixed Annuities

Of the its guaranteed development from built up passion settlements stands apart. Repaired interest rates offer small development in exchange for their guaranteed profits. You potentially can make extra long term by taking added risk with a variable annuity, but you might likewise lose cash. While repaired annuity contracts stay clear of market threat, their trade-off is less growth potential.

Spending your variable annuity in equity funds will supply more prospective for gains. The charges connected with variable annuities may be greater than for other annuities.

The insurer might enforce surrender costs, and the internal revenue service may levy an early withdrawal tax obligation charge. Give up charges are laid out in the agreement and can vary. They start at a particular percentage and after that decrease with time. For instance, the abandonment fine might be 10% in the very first year yet 9% the next.

Annuity earnings undergo a 10% very early withdrawal tax obligation fine if taken prior to you get to age 59 unless an exemption uses. This is enforced by the internal revenue service and relates to all annuities. Both taken care of and variable annuities supply alternatives for annuitizing your equilibrium and transforming it right into an ensured stream of life time income.

Exploring Variable Annuities Vs Fixed Annuities Everything You Need to Know About Financial Strategies Breaking Down the Basics of Deferred Annuity Vs Variable Annuity Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Matters for Retirement Planning How to Compare Different Investment Plans: Simplified Key Differences Between Different Financial Strategies Understanding the Rewards of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Fixed Indexed Annuity Vs Market-variable Annuity Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at Fixed Vs Variable Annuities

You might make a decision to make use of both fixed and variable annuities. If you're picking one over the various other, the distinctions issue: A might be a far better option than a variable annuity if you have a more conservative danger resistance and you look for foreseeable rate of interest and major security. A may be a far better option if you have a higher danger tolerance and desire the capacity for long-lasting market-based growth.

There are different kinds of annuities that are made to offer various purposes. A fixed annuity warranties repayment of a set quantity for the term of the agreement.

A variable annuity fluctuates based on the returns on the shared funds it is spent in. An instant annuity begins paying out as soon as the customer makes a lump-sum repayment to the insurance firm.

Annuities' returns can be either repaired or variable. With a repaired annuity, the insurance policy company assures the customer a certain payment at some future day.

{kind=link}

Table of Contents

Latest Posts

Understanding Financial Strategies A Closer Look at Deferred Annuity Vs Variable Annuity What Is What Is A Variable Annuity Vs A Fixed Annuity? Features of Smart Investment Choices Why Retirement Inco

Decoding Indexed Annuity Vs Fixed Annuity Key Insights on Indexed Annuity Vs Fixed Annuity Defining the Right Financial Strategy Pros and Cons of Various Financial Options Why Choosing the Right Finan

Highlighting Variable Vs Fixed Annuities A Closer Look at Immediate Fixed Annuity Vs Variable Annuity Breaking Down the Basics of Fixed Indexed Annuity Vs Market-variable Annuity Advantages and Disadv

More

Latest Posts